RESEARCH REPORT

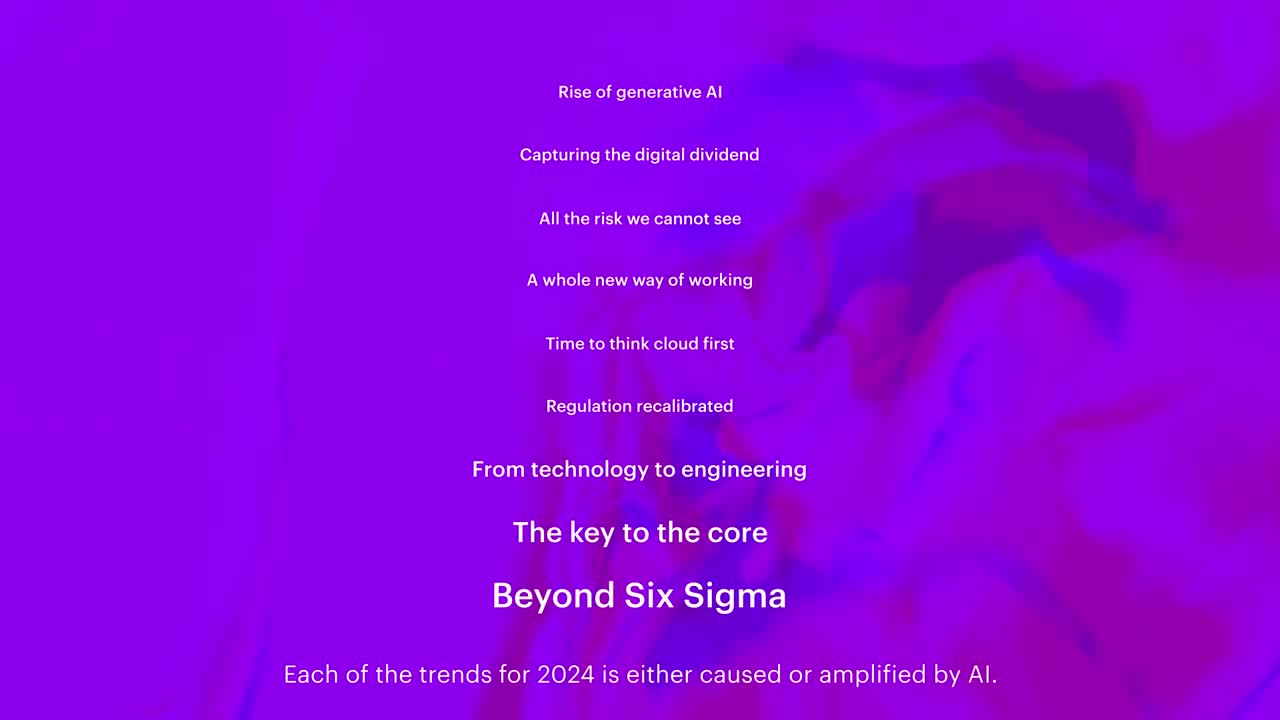

Top 10 banking trends for 2024

Banking on AI

5-MINUTE READ

January 7, 2024

RESEARCH REPORT

Banking on AI

5-MINUTE READ

January 7, 2024

A quarter of a century ago, banking stood on the verge of the Digital Age. The internet was starting to reveal its potential and most bankers had a strong premonition that far-reaching change was coming. Today we feel a similar sense of awe as we contemplate the potential of gen AI, especially when powered by the cloud and rapidly expanding data capabilities.

We’re confident the age of AI will change banking and many other industries—exactly how, we’ll only know in retrospect. No part of the bank—and few if any roles within it—will remain untouched.

Every year we share our perspective on the trends most likely to shape the future of the industry in the next 12 months and beyond. It should be no surprise the number one trend this year is the rapid adoption of gen AI, nor that it’ll have a transformative impact on the other nine trends bankers will need to confront in the months to come.

We’re now on the threshold of the Age of AI. Banking, like most other industries, will never be the same. The challenge is to ensure it’s a force for good that benefits our organizations, our people and all humankind.

Banks are likely to benefit more than other industries—our analysis indicates productivity could rise by 20–30% and revenue by 6%. Banks will need to not only utilize cloud and data effectively, but also to rethink work and talent.

While most banks have mastered digital, it has come at the cost of close customer relationships. Banks will need to focus on finding ways to have meaningful conversations with customers across these channels – AI may hold the key.

In 2024, banks will be confronted by a variety of risks—some familiar, others less obvious. We've identified five that deserve particular attention. Planning for the unplanned will pay dividends.

Banks are realizing that people are just as important as technology to the success of their human + machine initiatives. They’re putting talent at the center of their strategies as they reimagine the future of work.

Banks have always known optimized pricing can hugely impact their top and bottom lines. Now they’re starting to combine intuition with gen AI and more comprehensive data to turbocharge scenario planning and move closer to personalized pricing.

Most banks’ early experiences of cloud were like that of a novice driver put behind the wheel of a Ferrari: they tried to drive it like a family sedan. Lately they're moving up through the gears and discovering what cloud can really do for them.

Bank regulations have ballooned since the 2008/9 Financial Crisis. We expect more collaboration among banks, central banks and regulators to work more effectively together.

How does the role of technology in banking evolve? A subtle change, with major organizational implications: the shift from a technology management to an engineering mindset.

New approaches and technologies—not least of which is gen AI and its ability to swiftly convert outdated code—are combining to finally free banks from the limitations of their aging core systems.

Banks have historically employed re-engineering and cost-out thinking to optimize operations and experiences—the limitations were clear. Gen AI’s learning ability breaks this barrier and ushers in a new way of thinking that goes beyond Six Sigma.

Gen AI will undoubtedly be disruptive, but we’re confident that most of this will be positive. Our recent Art of AI Maturity survey on the topic—involving 1,600 C-suite executives at many of the world’s largest companies—found that 42% of those leading the way have already achieved a return on their AI investments that exceeds their expectations.

But the secret to these outcomes isn’t AI—it’s how it’s being used. It’s as much about people as it is about technology and as much about strategy as implementation. That’s a lot of balls to keep up in the air. But banks that master this juggling act will look back in years to come and toast to 2024.

As we enter the Age of AI, many bankers feel the same sense of awe that their counterparts did a quarter of a century ago as they stood on the verge of the Digital Age.

Michael Abbott / Global Banking Lead

Michael Abbott discusses how generative AI could reshape financial services in 2024 in this American Banker podcast.

The speed at which gen AI is being adopted by most organizations in nearly all industries, and the massive escalation of the power of the technology, are convincing indicators that it is here to stay—and will have a profound impact on banking.

Gen AI will make bank professionals more productive and improve the efficiency of banks’ operating model. However, we believe its biggest impact will be to increase revenue and loyalty by improving banks’ ability to understand and respond to individual customers’ intent and financial goals.

There are few functions and roles that will not be affected; our analysis indicates 73% of banking roles have a high potential to be either automated or augmented. We’ve already identified about 50 promising use cases for banks.

People should be at the very center of every gen AI strategy. New skills are needed to design, build, implement and train gen AI – banks will need to get used to a new way of working.