Blog

The US$50b clean energy opportunity in Southeast Asia

5-MINUTE READ

December 19, 2022

Blog

5-MINUTE READ

December 19, 2022

To make successful inroads into the region, companies will need to present a holistic value proposition, work with partners, and embark on digitalisation initiatives to accelerate the adoption of renewables.

The juxtaposition of rising energy demand with falling supply has set the stage for strong growth in Southeast Asia’s clean energy market, presenting renewable energy players with a US$50 billion opportunity by 2050[1].

A report by the International Energy Agency (IEA) projects that primary energy demand across the region will increase by 50-60% over the next two decades. However, supply side constraints loom as traditional energy production from oil, gas, and coal faces structural decline. For example, output from the main oil producers such as Indonesia and Malaysia is projected to fall from the current 2.3 million barrels a day to 1.5 million barrels by 2040[2] due to the continuous maturation of shallow water basins.

Without changes to the status quo, Southeast Asia will need to depend on imports to meet up to 90% of its energy needs by 2050[3]. This presents significant risks to energy security that countries will have to mitigate.

One solution to addressing the supply-demand imbalance lies in the transition to clean energy.

Many Southeast Asian governments are leaning towards clean energy and have declared net-zero targets in a concerted effort to phase out coal and other fossil fuels. To achieve these goals, renewables will have to step up to the plate to account for about 90% of capacity by 2050, with solar, wind and hydro leading the way[4]. It is important, therefore, for renewable energy players to act now and position themselves for growth opportunities across the energy value chain in the region.

However, the industry will have its task cut out with Southeast Asia’s energy market widely varied and fragmented. Each country has its own pathway and timeline to achieve the energy transition. For example, Indonesia is not yet able to deliver grid connectivity equally to its 17,000 islands, with inter-region electrification rate ranging from 50% in Papua to 100% in Java[5]. On the other hand, countries like Singapore and the Philippines are already exploring the carbon tax or carbon pricing mechanisms.

The region is also notoriously difficult to navigate. Renewable energy policies are still largely in development, leading to ambiguity over the go-to-market and project development process.

Land ownership is often fragmented across multiple owners, so the acquisition of large parcels of land required for renewables, especially wind and solar projects, will be a complex and protracted process.

In some countries, foreign ownership laws limit the amount of investment by foreign entities. Malaysia, for example, requires foreign ownership to be limited to 49% before a business can benefit from the feed-in-tariff (FiT) scheme.

With intensive upfront capital investment required for renewable energy projects, financing is another big challenge facing developers. Standard power purchase agreements with public utilities across the region can carry lopsided risks with investors and financiers taking on more uncertainty, which diminishes their investment appetite.

Projects also need to be scalable and of a sufficient size to be viable and to qualify for suitable financing solutions. Yet at the same time, the levelised cost of electricity is still 30% higher than coal in Southeast Asia[6], which is a significant barrier to the adoption of renewables at scale.

So, what does it take for renewable energy players to succeed?

A key transformative enabler for the renewable energy industry is the adoption of a holistic value architecture that evaluates potential energy solutions from an economic, environmental, social, and technical perspective and aligns these with market needs and requirements.

Instead of focusing on cost as the key driver for decision-making when investing in low carbon initiatives, Accenture works with renewable energy players to highlight a broader range of benefits, for example, solutions and actions that not only reduce emissions but also help deliver system value[7] benefits such as job creation and health benefits from better air quality. This helps drive conversations around holistic value to make a case for change with all relevant stakeholders.

To cater to the different transition paths towards clean energy, we also help renewable energy companies to develop differentiated project offerings by embedding economic, environmental, social, and technical outcomes, providing each market with a set of solutions that is tailored to its current needs.

Strategic partnerships with different parties in the ecosystem - such as such as governments, other energy companies, financiers, startups, and industrial companies - are key to overcoming challenges arising from the fragmented Southeast Asia landscape and unlocking the value behind renewable energy investments.

For example, partnering with local players can help renewable energy companies to overcome roadblocks such as foreign ownership limitations and allow them to tap into local knowledge, relationships, and networks to unlock new opportunities for low carbon industrial projects. Companies can also work closely with governments to achieve renewable energy targets and unlock system value benefits.

On the financing front, renewable energy companies like Vena Energy have raised green bonds to support the financing of their projects[8] from the likes of DBS, ING, MUFG, BNP Paribas and ABN AMRO. The Green Bond proceeds will be used to refinance existing corporate loans for their renewables projects, addressing the challenge of access to attractive financing solutions.

The cost difference between renewables and traditional energy sources remains a significant barrier to its adoption. End-to-end digitalisation across the design, build and operate phases of a renewable energy project, leveraging technologies such as robotics and drones, analytics, augmented reality/virtual reality, and the Internet of Things (IoT), will enable the industry to be much more competitive in this respect.

For example, we have implemented digital initiatives to help a multinational electric company optimise asset productivity, resulting in a 30% decrease in outages and a 20% reduction in operating costs. We used intelligent and remote asset management systems, equipped with robotics and smart devices to inspect electrical infrastructure, and integrated an IoT platform to enable activities such as inspection planning, routing, and monitoring and control. This automation of substation maintenance processes can be scaled to over 1,000 substations, has also driven other benefits in streamlining work and reducing workers’ exposure to risks.

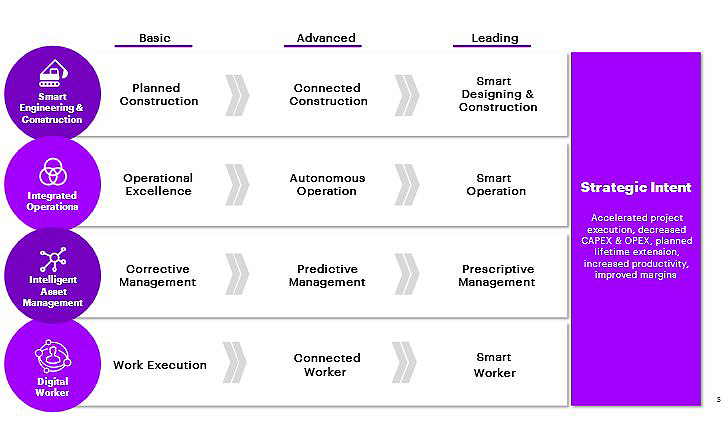

In terms of the digitalisation journey, there are four macro areas where we have focused on, to help renewable energy players reap the benefits of process efficiency, asset optimisation and cost reduction.

For example:

In smart engineering and construction, digital technologies can facilitate end-to-end project lifecycle management encompassing design and construction, supply chain and spare parts management and logistics optimisation by leveraging collaboration in the cloud.

Integrated operations will enable companies to leverage analytics for real-time insights to automate the control of assets and plants, and improve optimization through capabilities such as data-driven demand and supply matching and digital twins.

With intelligent asset management, renewable energy players will be able to use real-time operational data and analytics to intelligently manage and plan maintenance. This is possible with capabilities such as predictive maintenance for critical assets, predictive analytics for fault management, and prescriptive management through aerial thermography or automated plant performance diagnosis.

The fourth macro area is the digital worker, where digitalisation plays a key role in reducing reliance on on-site physical processes, while providing workers an access to timely insights for decision making.

Southeast Asia presents a huge opportunity that renewable energy players cannot afford to ignore. At the same time however, the highly diverse and fragmented market presents challenges for companies seeking to gain a foothold in the region, and the higher cost of renewables remains a barrier to its adoption.

To make an impact on the energy landscape, players will need to drive conversations around a new architecture of holistic value creation, build partnerships to navigate market penetration and financing challenges, and embark on digitalisation to improve the cost competitiveness of renewables and spearhead the region’s transition to clean energy.