This is the first in a series of in-depth thought leadership pieces on Open Banking in the Middle East. This one explains Open Banking and outlines key considerations for the Open Banking journey. Subsequent pieces will focus on the business case for banks in the region and lay out the actions they need to take – both technically and on the business side – in order to leverage Open Banking to best effect.

Open Banking is coming

- Open Banking is a fast-moving and increasingly important element of the banking industry in much of the world.

- Open Banking lets customers share access to their financial data with non-bank third parties via platforms. Third parties can use apps and services to provide customers with an “Uber-like” banking experience.

- With initiatives underway in the Middle East – for example, the issuance of guidelines by Saudi Arabia’s regulator – banks here need to prepare for its arrival.

- Factors driving Open Banking include regulatory policy developments, improved infrastructure, high rates of internet adoption and use of mobiles. The COVID-19 pandemic has accelerated the need to progress Open Banking.

Platforms and APIs are core

- Platforms are at the heart of Open Banking. Banks uncertain of the worth of platforms need to look only at the world’s most valuable firms like Amazon and Facebook.

- To succeed in Open Banking, banks in Saudi Arabia and the UAE, in particular, should start thinking like platform companies, flexing their business models to connect people and processes with assets, and backing that up with technology infrastructure that can manage interactions from internal and external users.

- At the heart of those interactions are application programming interfaces (APIs). These allow a direct connection between a customer’s bank account and a range of related services that can be provided by banks or by third parties.

- The API economy can bring significant revenue streams. APIs allow banks to charge for services that they offer through Open Banking or can be leveraged to cut costs, up-sell or cross-sell.

- There are numerous use cases for Open Banking, with more arising all the time. Some common use cases include seamless KYC processes; ecosystems in which APIs let customers link accounts across different banks, and which generate personal finance recommendations; bespoke services; and fraud prevention.

- Payments are a crucial aspect of Open Banking – and one in which significant work has already been done, with, for example, Saudi Arabia and the UAE laying payment rails.

- Real-time payments are another potential addition to the Open Banking space, with areas of interest including customer-facing services like corporate treasury; payment services providers (PSPs); acting as technology providers for merchants and other corporates; and operating Request to Pay (RTP) services.

How to start the Open Banking journey

- Banks looking to embark on their Open Banking journey have two choices: create their own ecosystem or join an existing one. Each has its benefits and drawbacks.

- Those looking to build their own Open Banking offering can consider off-the-shelf options.

- Banks can also take steps to advance the API and TPP spaces – for example, investing in developer portals and the developer experience to encouraging partnering on solutions.

- Regulators have a vital role in Open Banking and can employ various levers to mandate or encourage its development. Among the regional leaders are the regulators in Saudi Arabia and Bahrain.

- One key area for regulators involves APIs. Here they can work with the industry to guide the development of key APIs, set standards and establish uniform key performance indicators that govern API performance. Another area is TPPs, where regulators can ensure a standardised registration and licencing process.

- Although Open Banking is a work-in-progress globally, it is already revolutionising the industry. Banks in Middle East nations like the UAE and Saudi Arabia that want to stay relevant need to start positioning themselves by developing an Open Banking strategy. For many, that starts by seeing what peers elsewhere have done.

Open Banking: An integrated future in prospect

Open Banking has gained momentum in many countries in recent years, making it a core element in the digitalisation of financial services. Its growing popularity is little surprise, given how beneficial Open Banking is for customers, banks, government agencies and third parties.

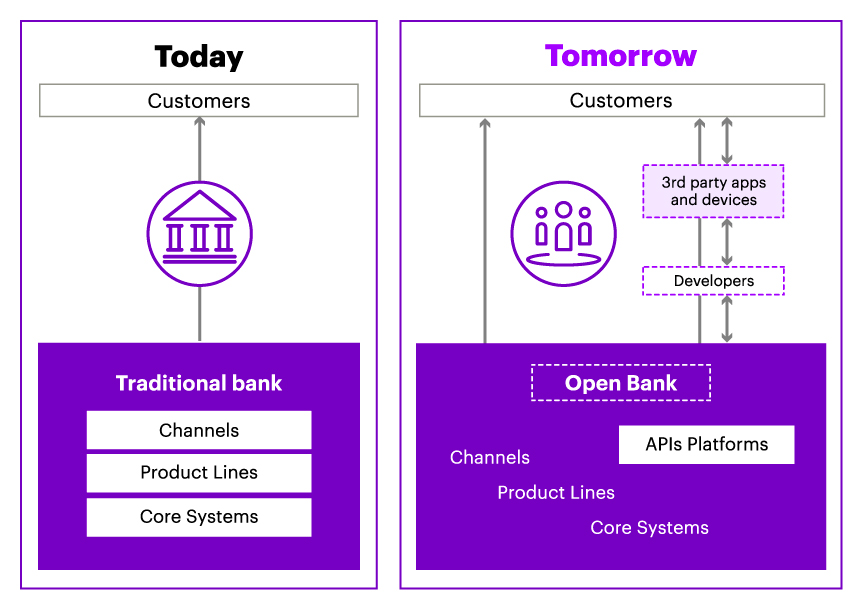

Open Banking lets customers share access to their financial data with non-bank third parties, who can then provide those customers with an “Uber-like” banking experience through the use of apps and services (see graphic).

The bank of today versus the bank of tomorrow: Open Banking in action. (Source: Accenture)

In some markets, Open Banking’s growth is due mainly to regulatory action (the EU and the UK, for example), while in others it has evolved naturally as market forces have dictated. Regardless of how it’s grown, the fact is that Open Banking is well-established in many regions.

That’s less the case in the Middle East, though, where Open Banking is largely in its infancy. Some countries do stand out: among the leaders is Bahrain, whose regulator started its Open Banking journey in 2018, and which issued a Bahrain Open Banking framework in 2020. Another is Saudi Arabia, which plans to launch Open Banking in the first half of 2022. Meantime, its central bank is working on its Open Banking policy, as well as on the design and implementation of an Open Banking ecosystem.

Where the Middle East will mirror other markets is in Open Banking’s requirement for multiple stakeholders. Regulators, of course, are key to its development. Banks will want to be at the core of Open Banking offerings, while third parties and aggregators round out the list of key players.

Beyond this central pool of players is the vast number of participants in Open Banking ecosystems, including governments and related public entities, companies, organisations and consumers. This process is underway in countries like Saudi Arabia, the UAE and Bahrain, and will soon be embarked upon by others in the region.

Key drivers

A number of factors are driving the adoption of Open Banking in the Middle East. Most obviously, there is the impact of the COVID-19 pandemic, which has accelerated the drive towards digitalisation for banks and regulators alike.

Yet local policies are also playing an important part. Saudi Arabia, for example, is implementing a cashless agenda and aims to make 70 percent of transactions non-cash by 2030. Several key infrastructure projects are underway, including the digital rails that will allow real-time payments (such as Saudi Arabia’s SARIE system), and which provide a way for people and firms to send and receive funds securely. Saudi Arabia leads in this area with Saudi Payments; we are given to understand that the UAE’s central bank is also planning a similar scheme.

The region’s high level of internet penetration and mobile phone usage, and a population that embraces digital solutions, are supporting factors. World Bank figures show, for instance, that the UAE has one of the highest rates of internet penetration in the world at 99 percent, while its mobile phone penetration rate is 200 percent. Saudi Arabia isn’t far behind, with rates of 96 percent and 120 percent respectively.

In addition, recent years have seen greater collaboration between countries in the financial services sector, with the UAE and Saudi Arabia’s work on the viability of a single dual-issued digital currency for domestic and cross-border payments (“Project Aber”) among the best-known.

In short, an array of factors has come together in the region, and the time is ripe for Open Banking to move ahead, underpinned by a foundation of robust security, centralised infrastructure and – in areas that are deemed suitable – stringent regulatory oversight.

A number of fintechs have pushed forward with their plans in recognition of these supporting factors and the value that Open Banking will bring (see box) – particularly in Bahrain, Saudi Arabia and the UAE. Use cases include payments solutions based on application programming interfaces (APIs) that allow a direct connection between a customer’s bank account and a range of related services.

Tarabut Gateway: Regional trailblazer

Tarabut Gateway is a Bahrain-based organisation that connects banks and fintechs through its single universal Open Banking API.

It went live in December 2019, and is not only one of the largest Open Banking infrastructure providers in the Middle East and North Africa (MENA) region; it is also the region’s first licenced Account Information Service Provider (AISP) and Payment Initiation Service Provider (PISP).

Its API supports firms in accessing a network of banks and fintech firms around the world, ensuring that funds and information can “flow securely, instantly and at a low cost”.

Open Banking: The road to adoption

The trajectory towards an Open Banking environment in the Middle East means traditional banks face a future of massive change. Understanding what to do starts by grasping that Open Banking is platform-based – an approach that has wholly upended other industries.

Outside of banking, the likes of Alibaba, Alphabet (Google’s parent company), Amazon, Apple and Facebook have unleashed the power of platform-based technology to remake the world. In doing so they’ve developed business models that provide customers with seamless digital experiences that integrate multiple ecosystems. This has blurred the lines between formerly separate industries and heightened consumer expectations about what is possible in terms of services and products.

Within the banking sphere, Open Banking’s platform-based approach has developed in one of two ways:

- The first, as seen in the EU and Australia, is the use of APIs to connect banks individually with aggregators, lenders, payments firms and other fintechs.

- The second, favoured by Singapore and Switzerland, is the use of a central API to which all parties, including banks, connect.

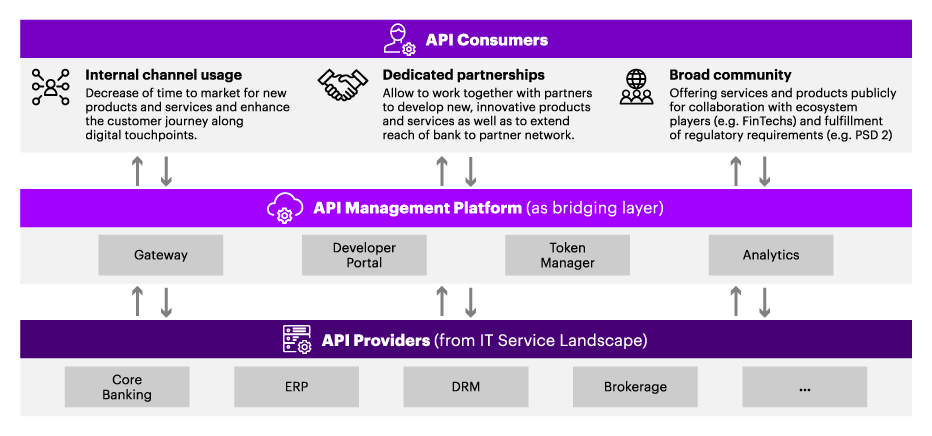

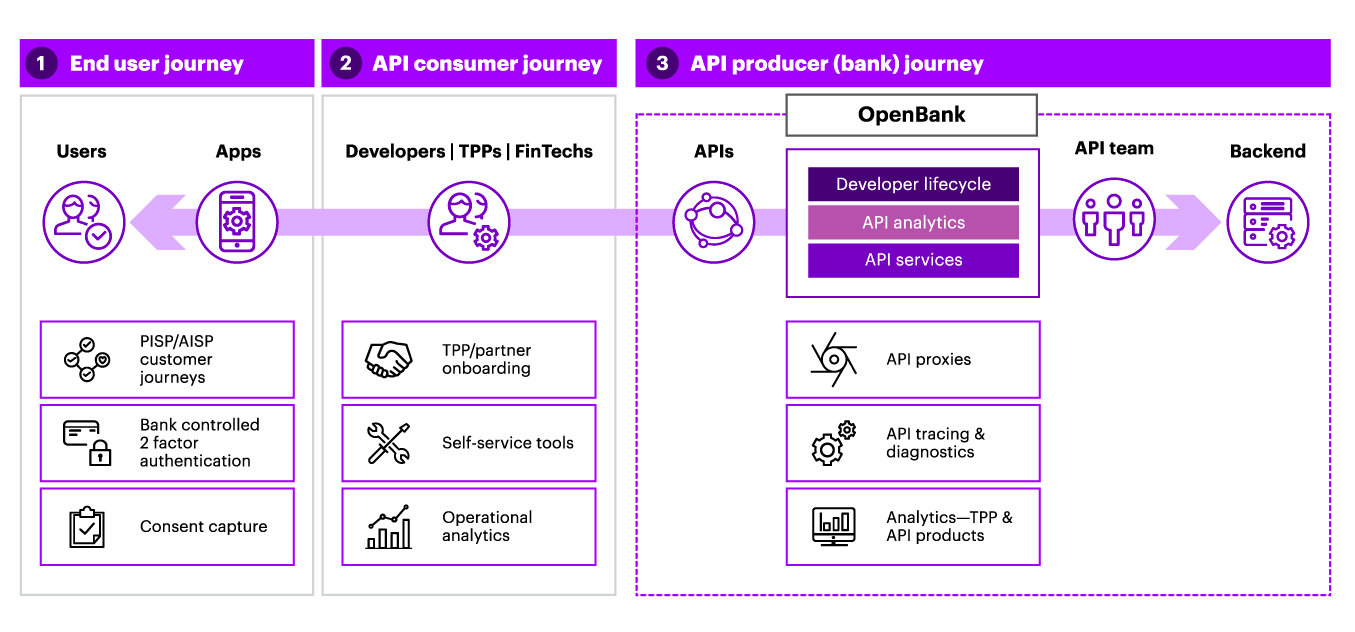

What’s common to both is a consistent API management platform that connects consumers with service providers, enabling and accelerating an open digital economy (see graphic).

API management – the bridge between consumers and service providers. (Source: Accenture)

The upshot for banks in the Middle East is that they need to start thinking like platform companies, with business models that connect people and processes with assets, and a technology infrastructure that manages internal and external users’ interactions.

It’s at this point in our conversations with banks that we’re typically asked the following:

- What are the optimal use cases for Open Banking at this stage for banks in Saudi Arabia and the UAE?

- How can I adopt an Open API ecosystem?

That’s what we’ll turn to next.

Use cases

As Open Banking has a vast number of use cases – with more emerging by the month – this section will examine just a few. One of the most common is an ecosystem within which every financial services participant can access KYC information. That removes the need for each to undertake their own laborious checks.

How might this work in practice? A telecoms firm providing a new mobile connection could use that ecosystem to access an individual’s information from a government agency for its KYC check. And a bank wishing to onboard the same customer could connect to this ecosystem to validate their details for KYC purposes via API calls with the telecoms provider. The result: a less costly, more efficient KYC process for all.

Another use case is an ecosystem via which bank customers use APIs to link all relevant accounts across different banks. In this way, Customer A could view a dashboard that contains all of their financial information in one place – including their savings account, credit card account, investment account and mortgage, for example.

That service could also be provided by a third party, which charges a fee, and from which Customer A benefits by receiving personal finance recommendations on steps that they could take to, for example, earn a better interest rate on their savings or benefit from lower investing fees – or that third party could provide other cross-sell products and services.

It could also see the bank or a third-party provider (TPP) offer a service that analyses Customer A’s portfolio across their different banks, and then uses analytics to deliver proactive, bespoke services based on that customer’s needs. Loyalty programmes are another area where we can see Open Banking playing its part.

These are examples of some of the most common use cases, but there are many others (see box), and more will emerge in the future.

What’s vital for banks to understand (and as our colleagues have written elsewhere) is that this API economy brings the opportunity to capture significant new revenue streams: banks can charge directly for services offered through Open Banking, or they can leverage APIs to cross-sell, up-sell or cut costs. And, importantly, this data-sharing via APIs is not a one-way street; instead, it goes both ways – from TPPs to banks and vice versa.

As we’ll see shortly, banks have a choice in how to approach Open Banking: participate in existing ecosystems or establish their own; either way, this approach will help them to create new revenue pools. Importantly, though, banks that position themselves at the core of this ecosystem will retain and own the customer relationship and experience.

How APIs cut fraud and monitor asset quality

Keeping a close check on asset quality is a key consideration for banks. Take the credit risk process, for instance. For banks in the Middle East, this can at times be an inefficient, time-consuming and relatively costly process. Many banks tend to require paper copies of bank statements, yet these can be easily manipulated.

A far better solution is to get the required information from a credible source digitally using APIs. Doing so brings numerous benefits: it cuts the potential for fraud, lowers costs, speeds processing times, and improves the customer experience.

An additional consideration is a risk that the quality of assets held by some banks in the region could deteriorate. Banks can ameliorate that risk by using APIs to leverage real-time or near-real-time data from internal and external sources, and integrate those into, for example, an early-warning signalling system.

Doing so would not only give banks the option to use multiple sources of data to monitor that risk; generating it in this way would preclude them from having to convince customers to share such data in the first place.

Banks could also apply the API-driven ecosystem principle to another key area of business: lending. It’s possible to automate the entire lending process by leveraging Open APIs and combine that with technologies like AI, machine learning and robotics.

However, to date, many traditional banks in the Middle East haven’t taken this approach – in some cases because they believe Open Banking is just for digital banks, neobanks or fintechs. It isn’t. The fact is that traditional banks must move into this space or risk losing market share.

Indeed, the urgency to act is compounded by the other challenges facing banks. COVID-19’s impact is one, but there are others: lower oil prices, for example, and a difficult business and operating environment. All of this means optimising costs has also become increasingly important.

The train is on the (payments) rails

Payments comprise a crucial area of Open Banking, and we noted earlier that important work on instant payments has been done in the region – particularly in Saudi Arabia and the UAE. With national players laying the rails, the time is ripe for banks to leverage the benefits that Open APIs bring.

Our colleagues in Europe have described Open Banking and real-time payments as “a match made in heaven” for banks. That’s true for banks in the Middle East too, with four main areas of interest:

- Customer-facing services: One example here is corporate treasury customers. In 2019, Deutsche Bank and software firm Serrala launched an API interface for the EU’s SEPA instant payments system that lets companies instantly initiate and process payments 24/7 through their SAP ERP system. Banks looking to enter this space will need to develop solutions for SMEs and corporates in, for instance, the accounting and payments-processing arenas.

- Payment Services Provider (PSP): Ant Financial, Square and Klarna are just three platform players that have disrupted this area with solutions that let customers use online banking credentials for instant payments and e-commerce. To compete, banks could also offer account-based e-commerce acceptance, as well as develop merchant-acquiring solutions that are based on account-to-account transfers.

- Technology provider for merchants and other corporates: PSPs run their own core payments services; some “white label” their infrastructure so that corporate clients can use it to manage access to accounts, identity services, and process payments. The account-to-account infrastructure used, for example, by Trustly, a fintech firm based in Sweden, lets customers pay merchants directly from their online bank account without using card networks.

- Request to Pay (RTP): this service is overlaid on instant payments and offers a more convenient and seamless user experience – with the beneficiary able to initiate a request for the payer to agree to a transfer of funds. Banks should keep in mind that retaining control of their RTP offering ensures they don’t lose that customer relationship.

Adopting an API ecosystem

It’s time to turn to the second question: How can my bank adopt an Open API ecosystem? As mentioned earlier, banks have two options:

- Create an ecosystem that has its bank at its heart; or

- Join an existing ecosystem.

The second option is clearly easier and would make sense for many banks. However, they should understand that this approach has some disadvantages, not least that their bank won’t control the ecosystem; instead, it will be simply one participant among many.

The only way to overcome that, of course, is to build one’s own ecosystem – and the fact that payments are at the heart of most ecosystems’ operations means that financial services firms (and banks in particular) have every reason to position themselves front and centre, leveraging Open APIs to connect the various participants and service providers. Building one’s own ecosystem means the bank continues to own the customer experience – and the valuable data that flows from those interactions.

How crucial is that? Well, earlier we noted that the world’s best-known ecosystems belong to firms like Facebook, Alibaba and Amazon, and it’s no coincidence that these are among the most valuable companies in history. Their ecosystems have had a huge amount to do with this success, allowing them to disrupt how other companies engage with and market to their clients and consumers in every part of the world.

That engagement and disruption are happening with Open Banking globally, and traditional banks in the Middle East will need to develop (or share in) such ecosystems if they wish, for example, to leverage banking APIs to best advantage. Should they fail to do so, other banking and non-banking players will move into this space. Indeed, that is already underway. March 2021 saw the launch of Dubai-based neobank YAP, which partnered with RAK Bank to offer services like remittances, spending and budgeting analytics, and P2P payments. The launch marks YAP’s first step in its bid to become a leader in this region and beyond.

What banks in the Middle East should keep in mind is that they don’t need to provide all of the services that an ecosystem offers – far from it. The purpose of the ecosystem is to create new revenue pools by connecting various stakeholders. Partnering with specialists that can provide value-adding services to the bank’s clients within that ecosystem context is key.

Let’s see how that might work in practice. Banks in, say, Saudi Arabia looking to build an ecosystem for companies could – and should – connect it to Saudi Payments’ Esal solution that covers e-invoicing and factoring, among other services. Similarly, banks can partner with fintechs for other cutting-edge solutions, creating the win-win-win that the global platform giants have shown is possible: satisfied customers, new revenue pools, and retention of the customer experience.

Regulatory levers, banking steps

A successful Open Banking system requires more than willingness from banks. Regulators, too, have a crucial role to play. For a start, it is the regulator’s role to ensure that appropriate checks are carried out before potential participants in the Open Banking system are awarded the relevant licences (such as for AISP or PISP services).

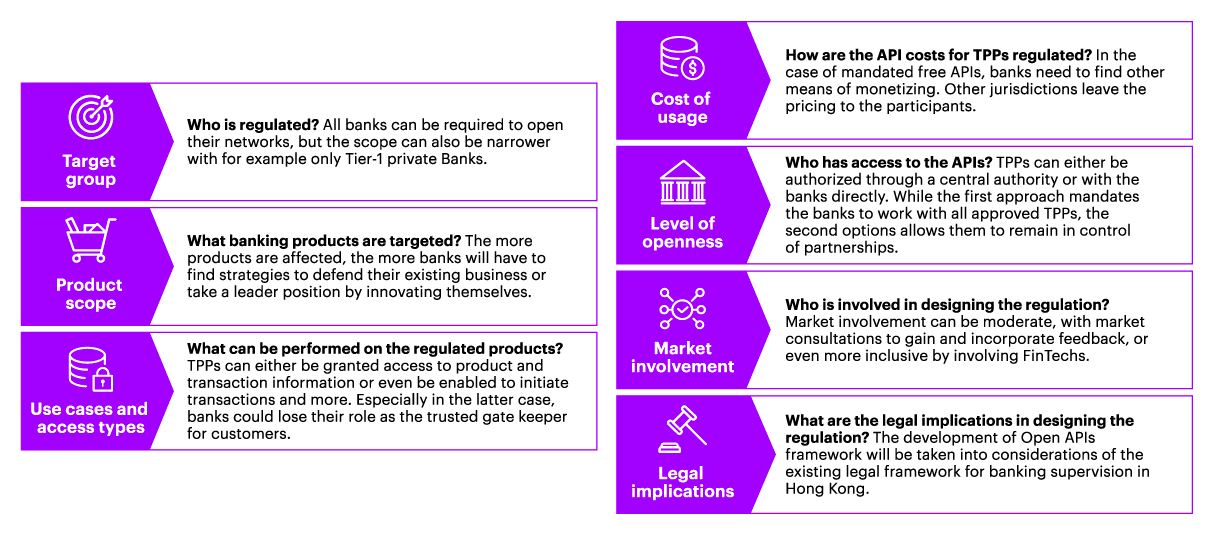

Also, as the infrastructure for Open Banking is built in the region, regulators can help by using levers to enable or mandate certain specific aspects (see graphic). Those levers can significantly affect the market dynamics, adoption rate and success of Open Banking.

Levers that regulators can use to influence Open Banking. (Source: Accenture)

Two important areas involve APIs and third-party providers (TPPs). Regulators can work with the industry to guide the development of key APIs, set API standards and establish uniform key performance indicators that govern APIs’ performance.

On the TPP front, there needs to be a standardised registration and licencing process, a TPP/API directory with information on bank API locations, and electronic certification to ensure secure identification of TPPs.

Other areas where regulators can play a crucial role include:

- Ensuring instant payments’ compatibility by mandating a standardised interface that connects with the existing instant payments infrastructure.

- API Aggregation/API Hub: this provides unified access to accounts, identity services and payments processing.

- Developing processes to handle unified incident reporting and dispute management.

At the same time, banks can take valuable steps in the API and TPP spaces – for example, investing in developer portals and the developer experience to provide a place within which developers can partner on solutions. Singapore’s DBS Bank is a leading example. Its DBS Developers platform has more than 200 APIs covering solutions including loans, rewards, fund transfers and deposits.

Banks will also need to address some important technical issues, including being able to deal with unpredictable volumes of traffic (cloud-based solutions are ideal for that), securing the high availability of APIs, and implementing robust, friction-free security.

API management solutions are also key as they can speed the building of APIs and linked solutions. Installing an API management layer or gateway ensures, among other things, that developers can create and configure APIs, and test them in a sandbox environment provided by the bank – as the DBS Developers platform does.

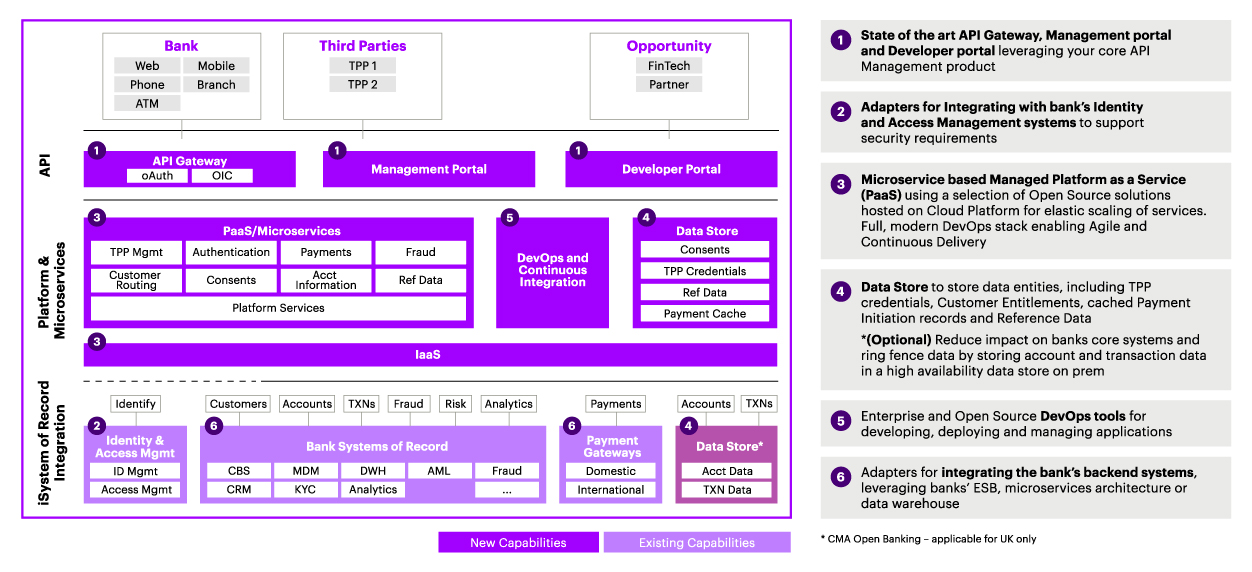

Banks that are unwilling or unable to build and integrate such solutions could consider off-the-shelf solutions, like Accenture’s “Open Banking in a Box” reference architecture that aims to provide full technical compliance, and that includes, among other aspects, an API gateway and microservice-based managed Platform as a Service (PaaS) that uses scalable, cloud-based, open-source solutions and a full DevOps stack (see graphic). Microservices include TPP management, authentication, payments, account information and fraud checks, to name just five.

Accenture’s “Open Banking in a Box” solution. (Source: Accenture)

Banks that are concerned about the challenges of building their own sandbox environment can also turn to off-the-shelf solutions that offer a self-contained, virtual environment that mimics live banking functionality. Sandboxes are core to fast-tracking API development, and banks can use this approach to ensure that APIs are rapidly created to meet business priorities (see graphic).

Key sandbox journeys that can ensure a secure space for market testing, digital innovation and ecosystem activation. (Source: Accenture)

Finally, regulators and banks alike need to factor in elements like data privacy and security. Banks, for example, need the consent of the end-customer if they are to share data under Open Banking, while regulators need to strike a balance between promoting Open Banking and ensuring that data privacy and security aren’t compromised. For both, aspects like authorisation and authentication are a core focus.

Open Banking is coming

Open Banking represents a paradigm shift for banks and the broader financial services industry, one that will change how banks view their business models, their service offerings and their competitors.

The key characteristics underpinning Open Banking are, naturally, openness (with banking services performed via non-banking channels and vice-versa); a platform-based approach that networks interlinked businesses with customers to create synergistic value; systematic regulation of those services and offerings; and the use of APIs as the enabling bridges between parties in this system.

Although Open Banking is in its adolescence globally – and in its infancy in the Middle East – it is already revolutionising the banking industry. The advantage for banks in this region is that they can look to, say, Europe, the UK, Singapore and Australia to see what their peers are doing, the trajectory of regulatory actions, and how the market is developing. That makes planning how to react a much simpler process.

For banks looking to stay relevant, that process can’t start soon enough. Comfortingly, the actions they should take aren’t limited by in-house capabilities, which means that even smaller banks can position themselves strongly for the future.

And, of course, banks and other players in the financial services industry should work closely with regulators and central banks as each country maps out its path. Being part of a collaborative conversation is important for everyone – after all, it’s essential that traditional banks, neobanks and fintechs alike understand the trajectory that Open Banking is taking in their markets in terms of regulation and initiatives.

Taking those first steps is similarly crucial. For banks, those revolve around determining where they stand on the subject, defining their Open Banking goals and constructing a route to success. For regulators, it’s deciding which levers they will use, the balance between mandating and guiding the development of Open Banking, and the extent of market involvement when designing regulations. For both, though, time is of the essence.

To download a copy of the Open Banking in the Middle East: Time is of the Essence report click here.